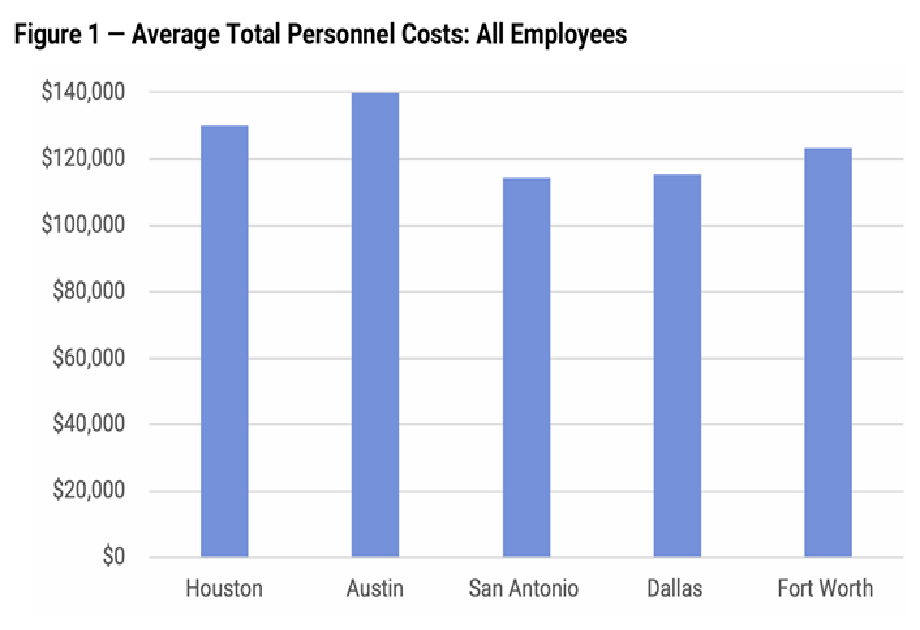

We now have audits for the City and its three pension plans for the first full year of operation under the pension changes made in 2017. The results clearly show that, other than making a one-time reduction in the pension liability by cutting benefits and increasing employee contributions, the changes did little to solve the long-term issues.

There are many metrics in the audits which support this view, but perhaps the clearest indicator is a comparison of the City’s total pension expense in 2016, the last year before the implementation of the changes, and this year’s result.[i]

Here are screenshots directly from the 2016 and 2018 audits.

So, after “solving the pension crisis,” the City’s pension expense has gone up by $70 million, a 7.9% increase.[ii] What a deal. By the way, it will likely be even higher in 2019 because all three plans are having a bad year in the markets. Under the accounting rules adopted a few years ago, the pension plans’ investment results flow directly into the calculation of the City’s pension expense.

The 2017 changes bought the City some time with the one-time reduction in the pension liability by cutting benefits and requiring employees to contribute more toward their retirements. But it did nothing to address the fundamental demographic issues all pension plans face or the moral hazard inherent in a system that allows politicians to promise benefits without being required to fully fund those benefits as they are incurred. Until we have the intestinal fortitude to have an honest discussion of those issues, the City will continue to stumble along from one pension crisis to another.

[i] The pension expense in 2017 includes the reduction in its pension expense from the reduction in benefits, and therefore, shows a negative pension expense of $1.2 billion. The pension expense in 2016 and 2018 are free of any extraordinary adjustments.

[ii] It is not clear from the audit, but it appears that the calculation on the net pension expenses does not included the interest on the $1 billion of pension bonds issued in 2017. If the interest on those bonds were included in the calculation (which it should be get an “apples-apples” comparison), the net pension expense for 2018 would have been approximately $40 million higher and the increase over 2016 would have been $110 million (12.5%).

.png)